This is an article from FT.

A hedgehopper's guide to living with inflation

Keynes' legacy is up for debate these days but there is almost universal sympathy for his scornful views of the long run. His dictums that in the long run we are all dead, and that the market can stay irrational longer than you can stay solvent, are unarguably true.

For those young enough, there is safety in the very long term. But those too old to wait around need help to hedge against the risk that things go wrong in the short run.

Here, miming the long-run data can still help. This week saw the publication of two annual monumental studies of long-term securities returns: the Barclays Equity Gilts Study and the Credit Suisse Global Investment Returns Yearbook. Both go back more than a century and cover many countries.

Mining such data can help us to deal with short-run risks and both surveys this year attempted to do so. On balance, their findings are still somewhat depressing but the condensed wisdom of a century is still useful.

First, equities do outperform in the long run term but that long term can indeed be very long. In the US, since 1900, the longest anyone has had to wait to derive a positive real turn from stock is 17 years (manageable for most of us); but, in Italy, that figure is 74 years.

How should those with time to wait best harness this insight? The Credit Suisse data confirm that stocks outperform if they are smaller (US micro-cap companies have grown at 12.6 per cent a year since 1926, compared with 12 per cent for small-capitalisation companies and 9.5 per cent for larger companies); if they are cheaper (higher dividend yield stock have risen at 10.9 per cent a year in the UK since 1900, compared with 7.7 per cent for low yielders); and if they have momentum at their back. Stocks that are rising tend to keep rising, and laggards tend to keep lagging. Place trades that take advantage of these inefficiencies and you will be rewarded in the long run.

What about those who cannot wait? The bad news from the Barclays survey is that safety has never been so expensive. Long-term interest rates on US sovereign debt are not unprecedentedly low. The forwards market, which institutions use to lock in interest rates for the future, shows that markets expect 10-year bond yields to average almost exactly 1 per cent from 2022 to 2032. Only 30 years ago, these bonds yields as much as 15 per cent.

Plainly, the intervention by central banks to push down yields by buying bonds has much to do with this. But the Federal Reserve is promising to keep rates low until 2014; that cannot explain such confidence they will stay low from 2022 to 2032. Barclays suggests the main explanation is shortage of supply. Since the financial crisis struck, several assets have been struck off the list of "safe" assets, such as US mortgage agency debt, structured credit, and Spanish and Italian bonds. For those safe assets that remain, this pushes up the price, while pushing down the yield.

Bonds are historically expensive relative to stocks. But if this is because of a permanent constriction in the supply of safe assets, these is no particular reason to expect this to change; and, therefor, sadly, it does not imply that stocks are particularly cheap.

Bonds' coupons are fixed over time, so a low long-term bond yield usually implies confidence that inflation will not rise and eat into their purchasing power. But in these circumstances, low bond yields do not imply any great market belief that inflation is under control.

Indeed, of course, there is great fear of inflation. What can act as a hedge? These days, inflaiton-linked bonds are available. They are extremely expensive, offering a negative yields, but they will rise with inflation as long as the issuing government avoids default.

The Credit Suisse survey looked at other possible inflation hedges. The results, shown in the chart, are discouraging. Equities are badly affected by bouts of inflation but do at least outperform bonds. Housing is much less affected. Gold is as close to an inflation hedge as the authors find out even here gold's performance in the long term is erratic. As its real (inflation-adjusted) price has differed substantially over time, it cannot be regarded as a good hedge.

For the short term, then, the long term has depressingly little encouragement. Safety is in short supply and expensive; stocks are not as cheap as they look and hedging against the risk of resurgent inflation in the future is very difficult.

It is best, for those who can, to hunker down in well-chosen equities for the longer term. For those who cannot, diversify as much as possible. from FT

2012/02/13

2012/02/05

ザ・スミスとマーケット

When good news is good news and so is bad news

I was looking for a job and then I found a job,

And heaven knows I'm miserable now.

-The Smiths, 1984

Sometimes it's heads I win, tails I win. The stock market rally of the past two months is real, and unmistakably being treated as such. The S&P 500 was yesterday up 25 per cent from its lowest point in October, satisfying the usual definition of a bull market. Mergers and acquisitions are starting to return after a long gap.

But this rally has been driven by two forces that tend to cancel each other out. One is the promise of easy money from central banks, which is often on hand to stave off a crisis or to jolt an economy out of a slump. The other is the belief that economies are faring better - which implies that markets are less likely to get their dose of easy money.

For this reason, markets often have a Smiths-like lugubrious reaction to positive economic news. But now markets are plugging in to an altogether trippier mode. It might even be possible, thanks to the way that European and US economic cycles have drifted apart, to have the best of both worlds; easier money in Europe and economic growth in the US.

US unemployment data are notoriously unreliable. But the January data, which saw 230,000 Americans join non-farm payrolls, while the unemployment rate fell to 8.3 per cent (it reached 10 per cent in 2009), cannot be explained away. Employment is expanding.

That makes the Federal Reserve less likely to resort to further quantitative easing (buying Treasury bonds to push down their yields and thereby lower interest rates for the economy as a whole). But risky assets are still doing well, perhaps because of optimism about Europe.

All is not well on the eurozone's periphery. Portuguese government bond yields surged to much the same levels that forced Greece to ask the EU for a second bail-out last year. Talks over how much of a hit banks should take in Greece's likely default next month have dragged on. And a European Central Bank report this week suggested an incipient credit crunch as banks tightened their lending standards.

And yet the mood surrounding Italy and Spain is upbeat. Anyone who bought the two countries' bonds when concern about the eurozone was at its most intense, in November last year, has made 20 per cent since then. Meanwhile, eurozone bank stocks are up 36 per cent since then.

The explanation takes only four letters: LTRO (long-term refinancing operation). It refers to the European Central Bank's offer to let banks borrow from it for three years using very generous collateral. When unveiled by Mario Draghi, the incoming ECB president, late last year, many were disappointed that he was not buying government bonds directly.

But now, traders believe the move cuts any risk of a "Lehman moment" drastically. In other words, if a European sovereign default was to happen, the chance of a cascading bank collapse in response is much reduced. And the total assets on the ECB's balance sheet have leapt by 44 per cent in six months. Maybe it will now resort to printing money. The short-term implications would be good for European banks.

To explain this rally using history, there are two decent recent parallels. In 2010, the first Greek bail-out and some insipid US economic data caused stocks and commodities to sell off. That was arrested in August of that year when Ben Bernanke of the Federal Reserve signalled that more quantitative easing was on the way.

Twice since 2008, in the springs of 2010 and 2011, US monthly jobs growth has exceeded 230,000. Both times it went on to fizzle. That fits the notion that after a financial crisis the economy is doomed to move sideways. Growth shifts in response to shifts in monetary policy.

A second analogy is more troublesome. After the meltdown of the Long-Term Capital Management hedge fund in 1998, which brought global credit markets to a standstill, there was a dramatic rally once the Federal Reserve decided to cut rates.

Traders believed this proved that central bank money would always be there to bail out ailing financial groups. The LTCM template was followed several times in the years before the Lehman disaster - for example, Fed intervention sparked rallies after the crises for Countrywide Financial in 2007 and Bear Sterns in early 2008.

At the moment, markets in Europe seem to be following the LTCM pattern. Having pushed up Italian and Spanish yields to unbearable levels, they have forced the ECB to act. Now they can party.

This is dangerous, even if it is more cheerful than listening to the Smiths. But the resumption of growth in the US, and the successful crisis management by the ECB, have bought much time for politicians to try to deal with the deeper problems of the eurozone. Let's hope they use it. from FT

I was looking for a job and then I found a job,

And heaven knows I'm miserable now.

-The Smiths, 1984

Sometimes it's heads I win, tails I win. The stock market rally of the past two months is real, and unmistakably being treated as such. The S&P 500 was yesterday up 25 per cent from its lowest point in October, satisfying the usual definition of a bull market. Mergers and acquisitions are starting to return after a long gap.

But this rally has been driven by two forces that tend to cancel each other out. One is the promise of easy money from central banks, which is often on hand to stave off a crisis or to jolt an economy out of a slump. The other is the belief that economies are faring better - which implies that markets are less likely to get their dose of easy money.

For this reason, markets often have a Smiths-like lugubrious reaction to positive economic news. But now markets are plugging in to an altogether trippier mode. It might even be possible, thanks to the way that European and US economic cycles have drifted apart, to have the best of both worlds; easier money in Europe and economic growth in the US.

US unemployment data are notoriously unreliable. But the January data, which saw 230,000 Americans join non-farm payrolls, while the unemployment rate fell to 8.3 per cent (it reached 10 per cent in 2009), cannot be explained away. Employment is expanding.

That makes the Federal Reserve less likely to resort to further quantitative easing (buying Treasury bonds to push down their yields and thereby lower interest rates for the economy as a whole). But risky assets are still doing well, perhaps because of optimism about Europe.

All is not well on the eurozone's periphery. Portuguese government bond yields surged to much the same levels that forced Greece to ask the EU for a second bail-out last year. Talks over how much of a hit banks should take in Greece's likely default next month have dragged on. And a European Central Bank report this week suggested an incipient credit crunch as banks tightened their lending standards.

And yet the mood surrounding Italy and Spain is upbeat. Anyone who bought the two countries' bonds when concern about the eurozone was at its most intense, in November last year, has made 20 per cent since then. Meanwhile, eurozone bank stocks are up 36 per cent since then.

The explanation takes only four letters: LTRO (long-term refinancing operation). It refers to the European Central Bank's offer to let banks borrow from it for three years using very generous collateral. When unveiled by Mario Draghi, the incoming ECB president, late last year, many were disappointed that he was not buying government bonds directly.

But now, traders believe the move cuts any risk of a "Lehman moment" drastically. In other words, if a European sovereign default was to happen, the chance of a cascading bank collapse in response is much reduced. And the total assets on the ECB's balance sheet have leapt by 44 per cent in six months. Maybe it will now resort to printing money. The short-term implications would be good for European banks.

To explain this rally using history, there are two decent recent parallels. In 2010, the first Greek bail-out and some insipid US economic data caused stocks and commodities to sell off. That was arrested in August of that year when Ben Bernanke of the Federal Reserve signalled that more quantitative easing was on the way.

Twice since 2008, in the springs of 2010 and 2011, US monthly jobs growth has exceeded 230,000. Both times it went on to fizzle. That fits the notion that after a financial crisis the economy is doomed to move sideways. Growth shifts in response to shifts in monetary policy.

A second analogy is more troublesome. After the meltdown of the Long-Term Capital Management hedge fund in 1998, which brought global credit markets to a standstill, there was a dramatic rally once the Federal Reserve decided to cut rates.

Traders believed this proved that central bank money would always be there to bail out ailing financial groups. The LTCM template was followed several times in the years before the Lehman disaster - for example, Fed intervention sparked rallies after the crises for Countrywide Financial in 2007 and Bear Sterns in early 2008.

At the moment, markets in Europe seem to be following the LTCM pattern. Having pushed up Italian and Spanish yields to unbearable levels, they have forced the ECB to act. Now they can party.

This is dangerous, even if it is more cheerful than listening to the Smiths. But the resumption of growth in the US, and the successful crisis management by the ECB, have bought much time for politicians to try to deal with the deeper problems of the eurozone. Let's hope they use it. from FT

2012/02/01

Cees Nooteboom on the Dutch city where centuries swirl in the twilight

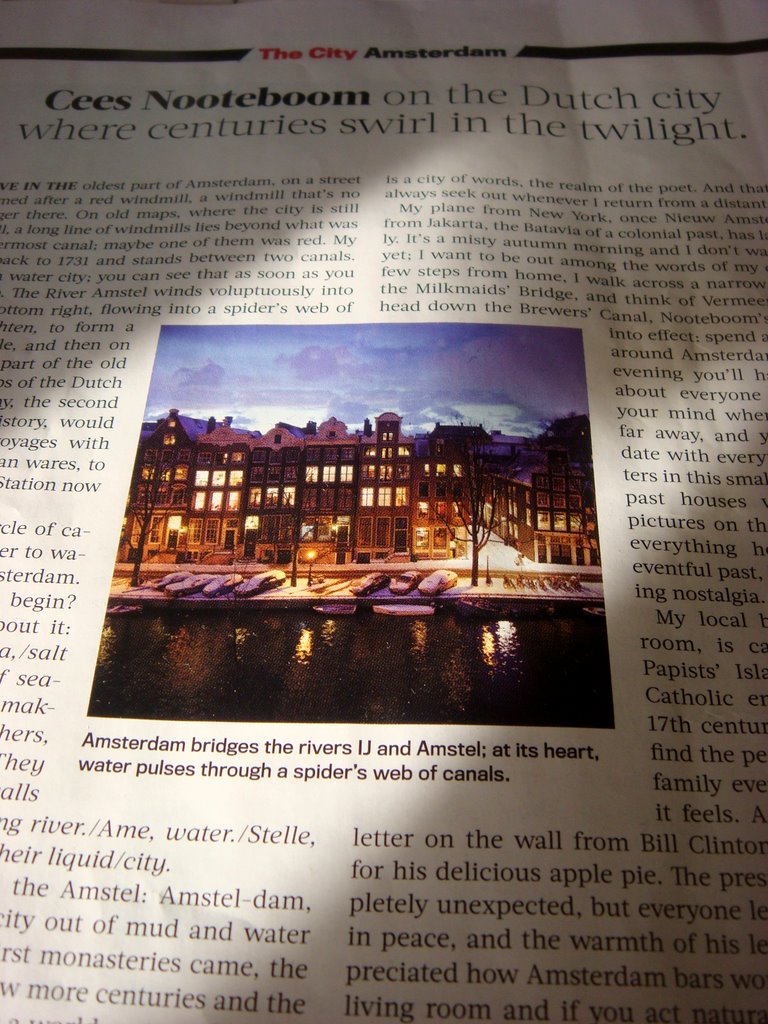

I live in the oldest part of Amsterdam, on a street named after a red windmill, a windmill that's no longer there. On old maps, where the city is still small, a long line of windmills lies beyond what was then the outermost canal; maybe one of them was red. My house dates back to 1731 and stands between two canals. Amsterdam's a water city; you can see that as soon as you open up a map. The River Amstel winds voluptuously into the city from bottom right, flowing into a spider's web of canals, or grachten, to form a magical semicircle, and then on into the River IJ, part of the old Zuiderzee. The ships of the Dutch East India Company, the second multinational in history, would return from long voyages with their Asian and African wares, to moor where Centraal Station now stands.

That magical semicircle of canals traveling from water to water is the heart of Amsterdam. But how did that city begin? I once wrote a poem about it: Between sea and sea, / salt marshes / behind dykes of seaweed. / Water people, land makers, / black angels, / forefathers, gliding over mud flats. / They are the first. / They dream walls of driftwood / in the wandering river./ Ame, water. /Stelle, place of safety. / The name of their liquid / city.

They made dykes, a dam in the Amstel: Amstel-dam, Amsterdam. They pulled that city out of mud and water and, a few centuries later, the first monasteries came, the first markets, the first ships. A few more centuries and the city on the IJ and the Amstel was a world metropolis, rich and powerful. Hundreds of ships anchored there, transferring their cargo onto smaller boats, which sailed into the city on an inland waterway that is both a labyrinth and an image of the highest order. The innermost circle, Singel, was once a defensive barrier against water and enemies. Then the second canal was dug, Herengracht, the gentlemen's canal, its name evidence of a new and assertive bourgeoisie. The princes and emperors came along later, in Prinsengracht and Keizersgracht, which are intersected by so many smaller grachten: canals of the tanners, the brewers, but also of the lilies, the laurels, and the elk, for this city is a city of words, the realm of the poet. And that's what I always seek out whenever I return from a distant journey.

My plane from New York, once Nieuw Amsterdam, or from Jakarta, the Batavia of a colonial past, has landed early. It's a misty autumn morning and I don't want to sleep yet; I want to be out among the words of my city. Only a few steps from home, I walk across a narrow footbridge, the Milkmaids' Bridge, and think of Vermeer. Then, as I head down the Brewers' Canal, Nooteboom's Law comes into effect: spend a day walking around Amsterdam and by the evening you'll have seen just about everyone who crossed your mind when you were so far away, and you'll be up to date with everything that matters in this small cosmos. I walk past houses with dates and pictures on their gable stones; everything here suggests an eventful past, but without cloying nostalgia.

My local bar, a dark living room, is called Papeneiland, Papists' Island, and it was a Catholic enclave back in the 17th century. It's where I go to find the people who are not my family even though that's how it feels. A recent addition is a letter on the wall from Bill Clinton, praising the owner for his delicious apple pie. The president's visit was completely unexpected, but everyone left him to enjoy his pie in peace, and the warmth of his letter shows that he appreciated how Amsterdam bars work; you're in someone's living room and if you act naturally, you'll find yourself among friends.

At the end of my day, I walk my poem to the beat of my feet, down a narrow alleyway called Prayer Without End (the site of a nunnery in the 14th century), through streets with names like Herring Sheds and Piggy-Bank Lane, and when I finally return home, I can feel the centuries swirling around my head, together with the light of this city on the water, the light you see in paintings from the Golden Age, a light that is found in no other place. from Newsweek

That magical semicircle of canals traveling from water to water is the heart of Amsterdam. But how did that city begin? I once wrote a poem about it: Between sea and sea, / salt marshes / behind dykes of seaweed. / Water people, land makers, / black angels, / forefathers, gliding over mud flats. / They are the first. / They dream walls of driftwood / in the wandering river./ Ame, water. /Stelle, place of safety. / The name of their liquid / city.

They made dykes, a dam in the Amstel: Amstel-dam, Amsterdam. They pulled that city out of mud and water and, a few centuries later, the first monasteries came, the first markets, the first ships. A few more centuries and the city on the IJ and the Amstel was a world metropolis, rich and powerful. Hundreds of ships anchored there, transferring their cargo onto smaller boats, which sailed into the city on an inland waterway that is both a labyrinth and an image of the highest order. The innermost circle, Singel, was once a defensive barrier against water and enemies. Then the second canal was dug, Herengracht, the gentlemen's canal, its name evidence of a new and assertive bourgeoisie. The princes and emperors came along later, in Prinsengracht and Keizersgracht, which are intersected by so many smaller grachten: canals of the tanners, the brewers, but also of the lilies, the laurels, and the elk, for this city is a city of words, the realm of the poet. And that's what I always seek out whenever I return from a distant journey.

My plane from New York, once Nieuw Amsterdam, or from Jakarta, the Batavia of a colonial past, has landed early. It's a misty autumn morning and I don't want to sleep yet; I want to be out among the words of my city. Only a few steps from home, I walk across a narrow footbridge, the Milkmaids' Bridge, and think of Vermeer. Then, as I head down the Brewers' Canal, Nooteboom's Law comes into effect: spend a day walking around Amsterdam and by the evening you'll have seen just about everyone who crossed your mind when you were so far away, and you'll be up to date with everything that matters in this small cosmos. I walk past houses with dates and pictures on their gable stones; everything here suggests an eventful past, but without cloying nostalgia.

My local bar, a dark living room, is called Papeneiland, Papists' Island, and it was a Catholic enclave back in the 17th century. It's where I go to find the people who are not my family even though that's how it feels. A recent addition is a letter on the wall from Bill Clinton, praising the owner for his delicious apple pie. The president's visit was completely unexpected, but everyone left him to enjoy his pie in peace, and the warmth of his letter shows that he appreciated how Amsterdam bars work; you're in someone's living room and if you act naturally, you'll find yourself among friends.

At the end of my day, I walk my poem to the beat of my feet, down a narrow alleyway called Prayer Without End (the site of a nunnery in the 14th century), through streets with names like Herring Sheds and Piggy-Bank Lane, and when I finally return home, I can feel the centuries swirling around my head, together with the light of this city on the water, the light you see in paintings from the Golden Age, a light that is found in no other place. from Newsweek

登録:

コメント (Atom)